Plutus OPE

Shouldn’t your software stack reflect the latest hardware? We’ve re-imagined high performance computing and applied it to derivatives. You should take a look…

Introducing: Plutus OPE

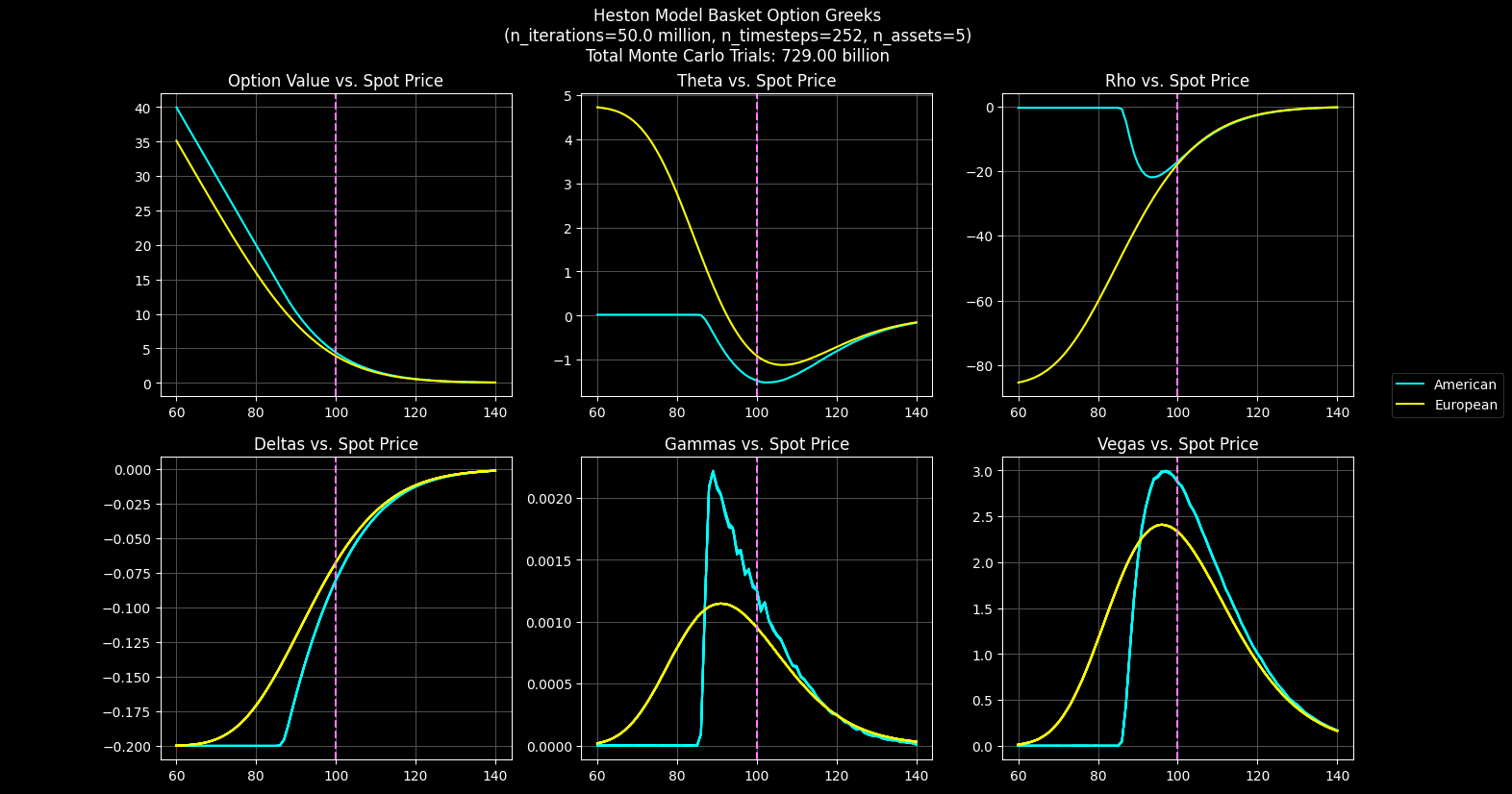

Supercharge your exotic options analysis with Plutus OPE. Over a billion Monte Carlo simulations per second. All with the confidence of a full Heston path model, using Longstaff Schwartz and Black-Scholes.

Advantages of Plutus OPE

• Fast, high accuracy exotic options pricing at up to one billion pricings per second

• OPE uses proven financial methodologies - Longstaff Schwartz, Heston path dependent pricings, and Black-Scholes

Features

• Build a portfolio using Plutus OPE or upload a pre-built portfolio using a Jupyter notebook

• Results include all first and second order derivative Greeks